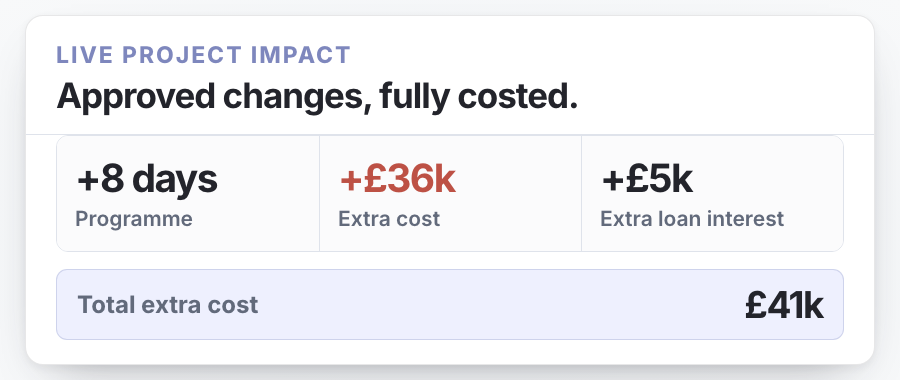

Kingsworth Gardens, Altrincham WA14

Drawdown DD-07

10 of 12 claim lines ready

This drawdown valuation

£121,790

Site progressThis drawdown

ItemEvidencePreviousThis drawOverallValuation

FrameComplete68%+7%75%£48,070

ElectricalRequired34%+9%43%£36,420

GlazingComplete55%+10%65%£21,300

LandscapingRequired12%+4%16%£16,000

Book QS visit

Send to QS portal

Finalise drawdown